Work Out How Much You Can Borrow

The Central Bank's mortgage rules set the hard limits, and they are simple for first-time buyers: you can borrow up to 4 times your gross annual income, and you need a deposit of at least 10% of the purchase price (a maximum loan-to-value of 90%).

A worked example. A couple earning €85,000 combined can borrow up to €340,000. Add their 10% deposit and their realistic price ceiling is roughly €377,000. A single buyer on €50,000 can borrow up to €200,000, for a budget of about €222,000 with the deposit.

Lenders can exceed these limits for a small share of applicants, but treat 4 times income as your planning number. Banks will also stress-test your repayments, so clean up your current account for six months before applying: no missed payments, no gambling transactions, and consistent savings.

Build Your Deposit and Budget for the Extra Costs

The deposit is not the only cash you need on the table. Budget around 12% of the purchase price in total to cover everything:

- Deposit — minimum 10% of the price.

- Stamp duty — 1% of the purchase price on homes up to €1 million.

- Legal fees — solicitors typically charge a flat fee or a small percentage; get two or three quotes before choosing, as prices vary widely.

- Valuation and survey — your lender requires a valuation, and a structural survey is strongly advised on second-hand homes.

On a €350,000 home that means a €35,000 deposit, €3,500 stamp duty, plus legal and survey costs on top — realistically €40,000–€42,000 in cash.

Claim the First-Time Buyer Schemes You're Entitled To

This is where Irish first-time buyers leave real money behind. Three schemes matter, and they can be combined in specific ways.

Help to Buy (HTB). A refund of the income tax and DIRT you paid over the previous four years, worth up to €30,000 or 10% of the purchase price, whichever is lower. It applies only to new builds and self-builds priced at €500,000 or less, and you must borrow at least 70% of the property's value. You commit to living in the home for five years, or Revenue can claw the relief back. The scheme has been extended to the end of 2029, so there is no need to panic-buy before a deadline.

First Home Scheme (FHS). The State takes an equity stake of up to 30% in your new home (up to 20% if you also use Help to Buy) to bridge the gap between your mortgage and the price. Local price ceilings apply — €500,000 for houses and apartments in Dublin city, Dún Laoghaire-Rathdown, Fingal, South Dublin, Wicklow and Cork city, and €475,000 in Galway city, Kildare and Meath, with ceilings reviewed twice a year. The stake is free for the first five years; from year six a service charge applies, and the euro value of the State's share rises and falls with your home's value. You can buy the stake back at any time.

Local Authority Home Loan. A State-backed mortgage for buyers who cannot get enough finance from banks. From April 2026 the income limit is €80,000 for a single applicant and €85,000 for joint applicants. You need proof of insufficient offers from two commercial lenders, two years of continuous employment, and repayments must stay under one-third of your household income.

The practical takeaway: on a qualifying new build you can stack Help to Buy and the First Home Scheme together, dramatically shrinking the deposit and mortgage you need. Second-hand buyers get neither, which is why the schemes have pushed so many first-time buyers toward new estates.

Buying and owning a home in Ireland — the complete guide

Get Mortgage Approval in Principle

Approval in Principle (AIP) is the lender's statement of what it will lend you, and estate agents will not take you seriously without it. It usually stays valid for six to twelve months depending on the lender.

Prepare six months of bank statements, payslips, your Employment Detail Summary from Revenue, proof of your deposit, and evidence of rent payments — consistent rent is strong proof you can handle repayments.

Rates matter enormously over 30 years. The sharpest rates start around 3.0% for energy-efficient homes with strong deposits, while most first-time buyers currently fix between roughly 3.3% and 3.8%; the average rate on new Irish mortgages was 3.53% in late 2025. A new build with a high BER rating usually qualifies for a lender's "green" rate — one more financial argument for new builds. On €300,000 over 30 years, the difference between 3.3% and 3.8% is roughly €80 a month, or about €30,000 over the loan's life.

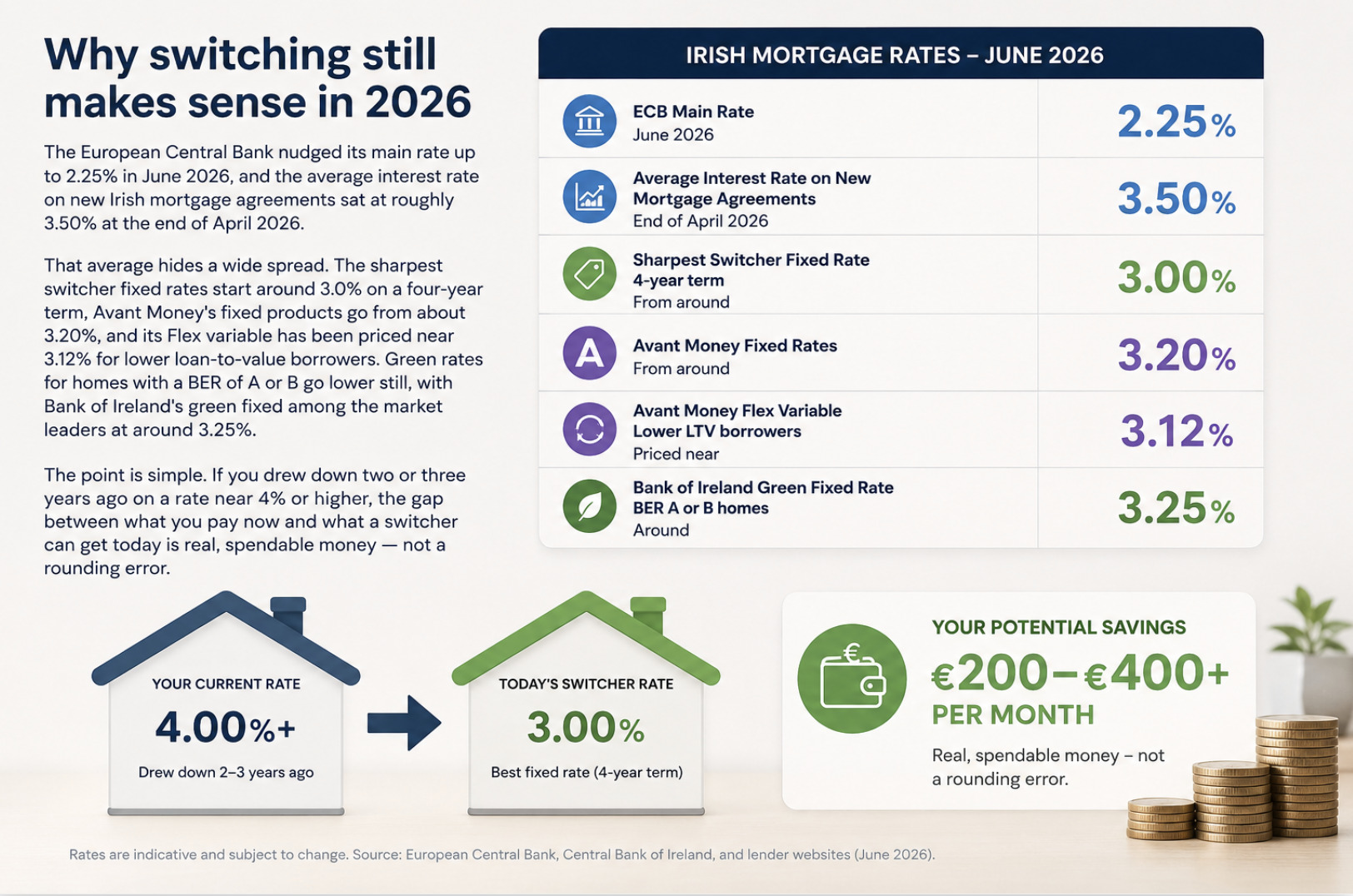

How to switch your mortgage in Ireland and save

Find the Home and Make an Offer

The market context: the median Irish home price is around €390,000, and in early 2026 completed sales were running about 7% above asking prices. Treat asking prices as a floor, not a ceiling, and set your search filters below your true maximum so you have bidding room.

When your offer is accepted you pay a booking deposit to the estate agent — typically a few thousand euro, and refundable until you sign contracts. The property is then "sale agreed", but nothing is binding yet for either side.

From Sale Agreed to Getting the Keys

Your solicitor now earns their fee: they investigate the title, raise queries, and review contracts. Your lender sends a valuer, and you'll need mortgage protection insurance and home insurance in place before drawdown — shop around for both rather than taking the lender's default offer.

For a new build, insist on a snag list: a professional inspection of unfinished or defective work the builder must fix before you close. Once contracts are signed and funds are drawn down, the balance transfers, stamp duty is paid, and you collect the keys. From sale agreed to keys typically takes a few months — longer for new builds still under construction, where Help to Buy and FHS paperwork also needs to align with the builder's schedule.

What SEAI grants are available and how to apply for them

Mistakes First-Time Buyers Should Avoid

Don't max out your bid at the very start of a bidding war. Don't skip the structural survey on a second-hand house to save a few hundred euro. Don't assume your own bank has the best rate — loyalty is expensive in Irish banking. And don't leave Help to Buy until the last minute: apply to Revenue early, because you'll need your HTB approval details when signing for a new build.

Ready to compare first-time buyer mortgage rates? The gap between the cheapest and dearest lender can be tens of thousands of euro over your mortgage. Compare current fixed and green rates side by side before you apply — it takes ten minutes and costs nothing. Compare mortgage rates now